by FTR | Sponsored Content, on Oct 08, 2023

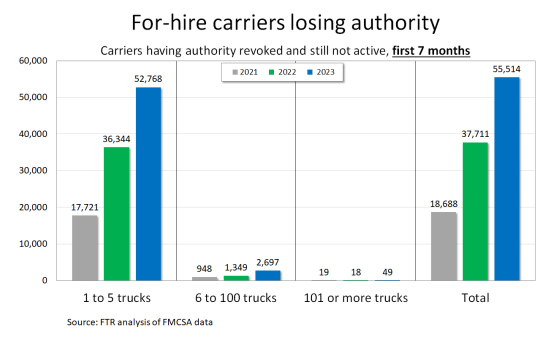

More than 55,000 carriers exited the market this year through July.

More than 55,000 carriers exited the market this year through July.

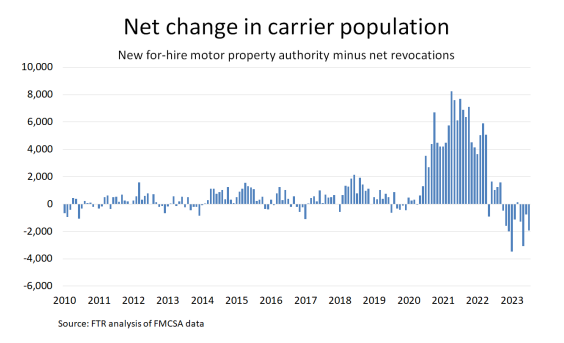

Since mid-2020, the trucking industry has seen a staggering period of entrepreneurship. Over the past 37 months, the Federal Motor Carrier Safety Administration (FMCSA) has authorized just under 288,000 new carriers. The largest number of new entrants approved during a 37-month period previously had been more than 130,000 between June 2017 and June 2020.

The number of new carriers authorized is still running around 1,000 a month more than the most recorded during a month before the pandemic, but the surge has been winding down for more than a year. Meanwhile, the number of carriers exiting the market has surged.

With higher net revocations – revocations of carrier authority minus reinstatements of authority – and fewer new carriers, the number of active for-hire trucking operations has been falling on a net basis since October 2022 aside from a tiny net increase in March. That 10-month period of decline is the longest by far since the Great Recession.

However, this downturn in the carrier population is not even close to reversing the 2020-2022 surge. As of July, the for-hire segment still had nearly 106,000 more carriers than it had in March 2020, an increase of more than 52%.

The following analysis addresses solely the gross numbers associated with carrier exits. In this commentary we are not attempting to adjust the figures for offsets, such as displaced drivers hired by other carriers or the number of new carriers entering the market, which is still high in historical terms as noted earlier. However, our July 2023 State of Freight Insights commentary does address the net change in driver capacity compared to the pre-pandemic period by comparing snapshots of registration data versus the figures for March 2020.

An Escalation of Carrier Failures

The number of carriers exiting the market does not mean much without the context of a “normal” period. To assess the most recent data available, we compared the first seven months of 2023 to the same periods during both 2022 and 2021.

The number of net revocations was already high by mid-2022, but the first seven months of 2021 was a period of strong spot rates and low diesel prices, so it is a good contrast for the like period this year.

According to FTR’s analysis of FMCSA data, during the first seven months of this year, 55,514 for-hire carriers gave up operating authority. The 2023 seven-month figure is about 47% above the same 2022 period and nearly three times the number of carriers that exited in the first seven months of 2021.

About 95% of carriers losing authority this year had fewer than six trucks, but the challenges are not limited to very small carriers. The number of carriers with more than 100 trucks exiting the market totaled 49, which is sharply higher than the fewer than 20 carriers in either the 2021 or 2022 periods.

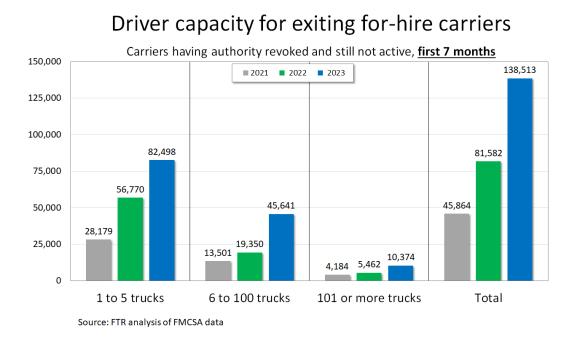

Not surprisingly, the smallest carriers’ share of drivers associated with failing carriers was not as large as their share of the number of carriers exiting. About 60% of the drivers associated with failing carriers worked for trucking operations that had fewer than six trucks. Carriers with six to 100 trucks accounted for about a third of drivers.

The average driver total for failing carriers has not changed that much during the period even though the number of larger carriers failing has risen sharply. The average during the first seven months of this year was about 2.5 drivers. During the same 2021 period, the average was 2.45 drivers. The outlier was 2022, during which the average failing carrier had 2.16 drivers.

The Path Ahead

The key question is whether the number of carrier exits will continue to grow or begin to settle. We cannot know for sure, but the underlying dynamics appear to support the notion that net revocations will be at least as strong as they are now for a while.

Two key factors are spot rates and diesel prices. Overall, spot rates probably have bottomed out, but the only segment that is seeing any real strength currently is refrigerated. Dry van spot rates are just barely rising, and flatbed rates have been declining for a full quarter.

We must acknowledge that these rate trends are mostly in keeping with seasonal expectations, at least directionally. However, trucking companies do not pay their bills with seasonal expectations. Sluggish rates are sluggish rates.

The more worrisome trend for carriers is the recent and ongoing surge in diesel prices. In general, this is a challenge primarily for the small carriers that operate mostly in the spot market and receive all-in rates without fuel surcharges.

With little freight strength anticipated, higher financing costs, and spot rates that do not seem poised for a surge, escalating diesel prices could be the catalyst for a surge in failures that could dwarf what we have seen to date. Even so, a substantial share of the pandemic-era shift likely is permanent.

Like this kind of content? Subscribe to our "Food For Thought" eNewsletter!

Now more than ever, professionals consume info on the go. Distributed twice monthly, our "Food For Thought" e-newsletter allows readers to stay informed about timely and relevant industry topics and FSA news whether they're in the office or on the road. Topics range from capacity, rates and supply chain disruption to multimodal transportation strategy, leveraging technology, and talent management and retention. Learn More